paulfromcamden

Baffled

You need to ask yourself for what are you investing. If its for retirement then its a no brainer to invest within a SIPP. Remember the tax

advantage on the money you invest 20% for a basic tax payer and 40% for a higher rate payer. Thats a 25% and 66% gain before you have bought anything!

For money you may need before then you invest in several ISA's over the years tax free. It all mounts up if you do the sums.

Cheers,

DV

I thought the advice was generally to max out the ISA allowance then put anything left in the SIPP.

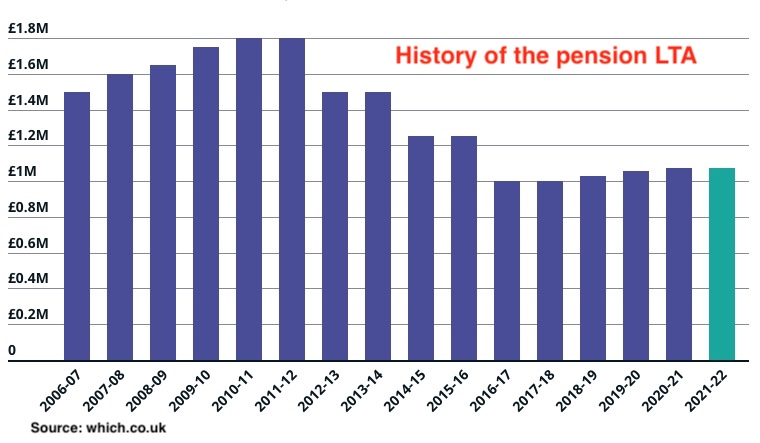

Income tax is payable on money withdrawn from a SIPP (plus there's the lifetime allowance).

An ISA is largely tax free, has no cap and can be accessed at any time.